Most executives remember with remarkable clarity the “woulda, coulda, shoulda” missteps made prior to the bear markets in 2000 and 2008.

Executives “woulda” navigated these markets with much less cost if they’d planned for ample liquidity. They “coulda” avoided selling company stock while it was down 20%, 30%, or 50% to fund their annual lifestyle. Their tax strategy “shoulda” been better so they wouldn’t have had to sell assets with high capital gains to increase liquidity during the bear market.

Furthermore, their financial plans “woulda” been more accurate if the incentive stock options “coulda” been monetized at 52-week highs. Instead, they watched the value vaporize as the stock traded down below the strike price of the options, which exponentially reduced their net worth picture.

Today, our relative-strength work firmly places our risk work on offense. The market is telling us that the current volatility is just that: volatile — and we believe it is not indicative of ominous trend changes in U.S. equity markets. Per our discipline, we follow the data and manage equity positions in our strategies. Our risk-on position is something executives may wish to consider adopting.

To be truly risk-on, we must consider the current context of the market. Where are our blind spots? What could we know, should we know, but have managed not to know? Answering these questions mandates further discussion of our asset-management strategy and how much of your capital is exposed to risk.

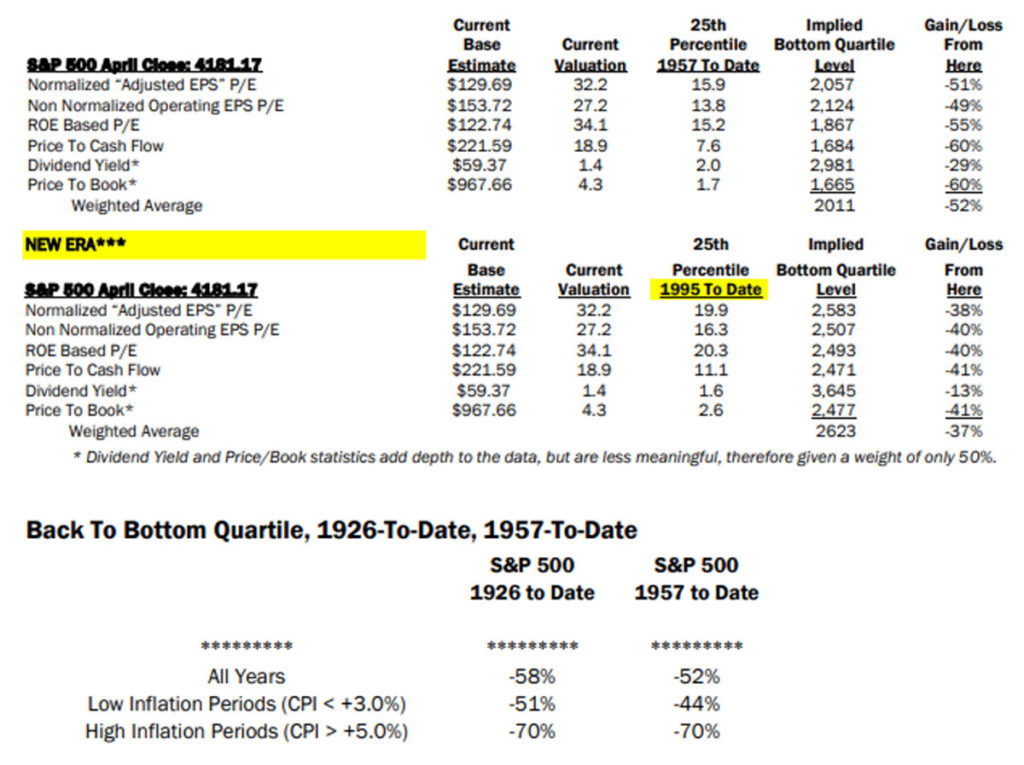

A respected thinker in this category, Doug Ramsey of the Leuthold Group, comments that secular bear markets drop well below median valuation levels. These itemized tables are based on a deterioration to the 25th percentile of the 1957-to-date historical distributions (all years regardless of inflation conditions). If the S&P 500 sank to the 25th percentile today, it would decline 52% (to 2,011). Using the 1995-to-date data, the indices would decline 37%.

To add some perspective, at the S&P 500 closing price low in March 2009, a 22% increase was needed just to rise up the 25th percentile of historical valuations.

Another respected thinker in this area is John Hussman of Hussman Funds. He writes the following:

“I can show, really precisely, that there are two warranted prices for a share. The one I prefer is based on such fundamentals as earnings and growth rates, but the bubble is rational in a certain sense. The expectation of growth produces the growth, which confirms the expectation; people will buy it because it went up. But once you are convinced that it is not growing anymore, nobody wants to hold a stock because it is overvalued. Everybody wants to get out and it collapses, beyond the fundamentals.” Nobel Laureate Franco Modigliani, New York Times, March 30, 2000

The word “bubble” is tossed around quite a bit in the financial markets, but it’s rarely used correctly. See, the thing that defines a bubble isn’t that valuations are extremely high, or that expected returns are extremely low. Instead, what defines a bubble is that investors drive valuations higher without simultaneously adjusting expectations for returns lower. That is, investors extrapolate past returns based on price behavior, even though those expectations are inconsistent with the returns that would equate price with discounted cash flows.

In March 2000, at the height of the technology bubble, I noted: “Over time, price/revenue ratios come back in line. Currently, that would imply an 83% plunge in tech stocks. If you understand values and market history, you know we’re not joking.” The following month, I discussed Modigliani’s quote above, and detailed the dynamics he was describing. The collapse of the 2000 bubble would ultimately erase half the value of the S&P 500 and would take the tech-heavy Nasdaq 100 down an implausibly precise 83%.

So how do we design strategies that respect polarizing perspectives of risk-on and the extreme valuations currently experienced? We do the work to extend our liquidity strategy and ensure we have ample liquidity for lifestyle needs over the next five, six, or seven years. This liquidity fortress helps reduce your risk of needing to sell assets with high capital gains when prices are low. Most importantly, there are no silos — it’s all connected.

To get started in positioning your risk-management strategy to be on offense during volatile market times, let’s set up a brief, 15-minute call.

Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor’s results will vary. Past performance does not guarantee future results.

The attached research DJIA research report was prepared and published by a third party, and is being provided to you by Raymond James Financial Services, Inc. solely for informative purposes. Any person receiving this report from Raymond James Financial Services Inc. and/or its affiliates should direct all questions and requests for additional information to their financial advisors and may not contact any analyst or representative of the third-party research provider. Neither Raymond James Financial Services, Inc. nor any third-party research provider is responsible for any action or inaction you may take as a result of reviewing this report or for the consequences of said action or inaction.

Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Past performance is not a guarantee of future results.

The Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stock of companies maintained and reviewed by the editors of the Wall Street Journal.

The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. The NASDAQ-100 (^NDX) is a stock market index made up of 103 equity securities issued by 100 of the largest non-financial companies listed on the NASDAQ. It is a modified capitalization-weighted index. … It is based on exchange, and it is not an index of U.S.-based companies.

Investing involves risk and you may incur a profit or loss regardless of strategy selected.